SEP IRA vs. Solo 401(k): What Self-Employed Business Owners Need to Know

Two of the most powerful retirement accounts available to self-employed individuals, but they work very differently. Here's how to think about which one fits your situation.

If you’re a solo business owner considering a SEP IRA or a Solo 401(k), this post will help explain:

How each account is structured

Key trade-offs between the two

What each option allows and what it doesn’t

How to think about which one fits your situation

The SEP IRA

The SEP IRA is one of the most straightforward retirement accounts available to self-employed individuals and small business owners. There’s no plan document to adopt, no annual IRS filings, and minimal ongoing maintenance. You can open one and fund it up to your tax filing deadline, which gives you significant flexibility if you’re making decisions late in the year.

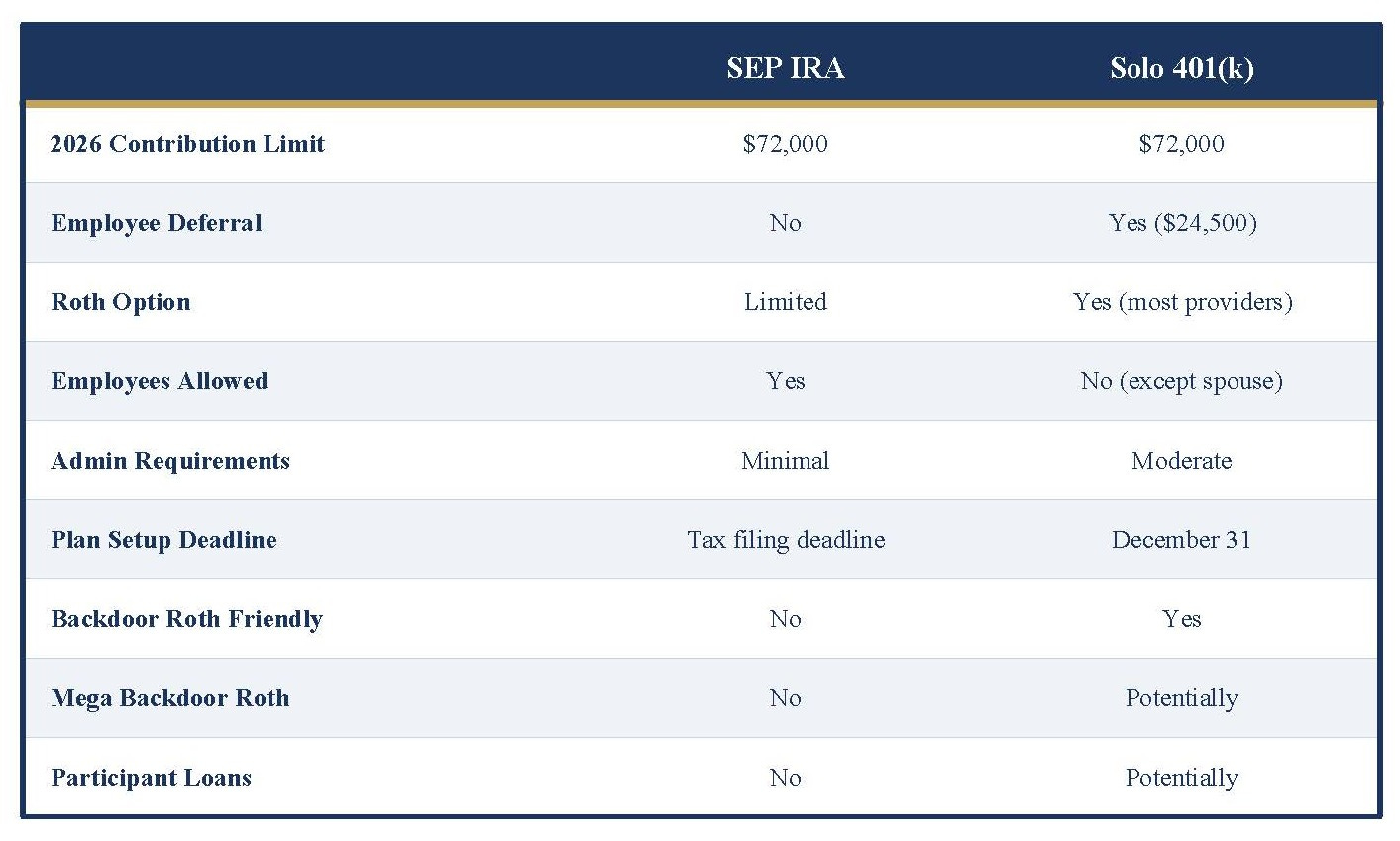

Contributions are made as the employer only, capped at 25% of net self-employment income up to $72,000 in 2026. One thing to keep in mind: if you have full-time W-2 employees, you’re required to contribute the same percentage of compensation for them that you contribute for yourself.

Where the SEP shines: Simplicity, flexibility on timing, and availability for businesses with employees.

Where it has limits: There’s no employee deferral component, so reaching the $72,000 ceiling requires roughly $288,000 in net self-employment income. At lower income levels, you may not be able to contribute as much as you would with a Solo 401(k). The SEP also has implications for certain tax strategies, which we’ll cover below.

The Solo 401(k)

The Solo 401(k), also called an Individual 401(k), is built exclusively for owner-only businesses. If you have full-time W-2 employees other than a spouse, you’re not eligible.

What distinguishes it is a two-layer contribution structure. You contribute as both the employee and the employer:

Employee deferral: up to $24,500 in 2026

Employer contribution: up to 25% of compensation

Combined max: $72,000 in 2026

Because the employee deferral is a flat dollar amount rather than a percentage of income, the Solo 401(k) can allow higher contributions at lower income levels. At $80,000 in net self-employment income, the employee deferral alone from the Solo 401(k) would be greater than the maximum allowable contribution to a SEP IRA. At higher income levels, the gap narrows and the two accounts become more similar in contributions they allow.

Where the Solo 401(k) shines: Higher contribution potential, Roth options, and compatibility with certain tax strategies.

Where it has limits: More administrative overhead and restricted to owner-only businesses.

The Admin Trade-Off

This is where the two accounts diverge most noticeably in practice.

The SEP IRA requires almost nothing ongoing. Open it, fund it, done. There’s no annual filing requirement and no setup deadline beyond your tax return due date.

The Solo 401(k) requires more. To make employee deferral contributions for a given tax year, the plan must be established by December 31 of that year. Missing that window means losing the employee deferral entirely for that year. Once plan assets exceed $250,000, you’re required to file a Form 5500-EZ with the IRS annually. You’ll also need to adopt a plan document at setup, though most major custodians provide one.

For someone who values simplicity and flexibility, the SEP’s lower maintenance can be a real advantage. For someone willing to manage the admin requirements in exchange for greater contribution flexibility and planning options, the Solo 401(k) can be worth the overhead.

Two Planning Considerations Worth Knowing

The Pro-Rata Rule and Backdoor Roth IRAs

If you’re a high earner doing, or interested in doing, backdoor Roth IRA contributions, the type of retirement account you hold matters. I covered the backdoor Roth in detail in a previous post.

In summary, the IRS applies what’s called the pro-rata rule when you convert IRA dollars to Roth. It treats all of your pre-tax IRA balances (Traditional, SEP, SIMPLE, and rollover) as one combined pool. If you have a large SEP IRA balance, a meaningful portion of any Roth conversion becomes taxable, which can significantly undermine the backdoor Roth strategy.

Pre-tax dollars inside a Solo 401(k) are not included in that calculation. This is a meaningful difference for high earners who want to keep the backdoor Roth on the table. If that strategy is part of your plan, it’s worth discussing with your CPA or financial advisor before defaulting to a SEP IRA.

The Mega Backdoor Roth

Some Solo 401(k) plans allow after-tax contributions beyond the standard employee deferral. If your plan permits it, you may be able to contribute after-tax dollars up to the $72,000 combined limit and then convert those dollars to Roth, either inside the plan or by rolling them to a Roth IRA. This is commonly referred to as the Mega Backdoor Roth.

This strategy isn’t available through a SEP IRA. But it also isn’t available through every Solo 401(k), it depends on whether your plan document allows after-tax contributions and in-plan conversions or in-service distributions. If this is something you’re interested in, it’s a question to ask before you open the account.

Side by Side Comparison

How to Think About Which One Fits

There’s no universal answer here. The right account depends on your income, whether you have employees, how you file your taxes, and whether strategies like the backdoor Roth are part of your financial plan.

The SEP IRA can be the better fit if you have employees, want to minimize complexity, or need the flexibility to decide late in the year. The Solo 401(k) can make more sense for owner-only businesses looking to maximize contributions or preserve access to Roth strategies.

One other difference worth knowing: Solo 401(k) plans that allow participant loans give you the ability to borrow from your own account, SEP IRAs don’t.

Either way, this is a decision worth making deliberately, ideally with your CPA and financial advisor.

Interested in learning more? Click Here to see what Dornick can do for you.

Dornick Wealth Management LLC (“Dornick”) is a registered investment advisor in Texas and other jurisdictions where exempted. Registration as an investment advisor does not imply any specific level of skill or training.

The content of this newsletter is for informational purposes only and does not constitute financial, investment, tax, legal, or accounting advice. While efforts are made to ensure accuracy, the information may not be complete, up to date, or applicable to your individual circumstances. It is not an offer or solicitation to buy or sell any securities or investments, nor does it endorse any specific company, security, or investment strategy. Readers should not rely on this content as the sole basis for any investment or financial decisions.

Past performance is not indicative of future results. Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategies discussed will result in profits or avoid losses.

All information is provided “as-is” without any warranties, express or implied. Dornick does not warrant the accuracy, completeness, or reliability of the information presented. Opinions expressed are those of the author, Levi Pettit, and are subject to change without notice.

No advisor-client or fiduciary relationship is formed by use of this blog or newsletter. For advice tailored to your personal situation, please consult with a qualified financial advisor, tax professional, or attorney.

Dornick is not responsible for any errors or omissions, nor for any direct, indirect, or consequential damages resulting from the use or reliance on this information. Use of the content is at your own risk. This content is not intended as an offer or solicitation in any jurisdiction where such an offer or solicitation would be illegal.